Written by : Terje. H Nilsen

Incorporating a company in Indonesia has never been easier.

With the Online Single Submission (OSS) system, a foreign investor can establish a PT PMA in a matter of days. In many cases, this process involves using a virtual office (VO) as the company’s registered address.

And from a legal standpoint, this is entirely permissible.

Under Law No. 40 of 2007 on Limited Liability Companies, every PT must have:

▪ A name

▪ A domicile

▪ A complete registered address

The law does not prohibit the use of a virtual office. In fact, more recent tax regulations — including Director General of Taxes Regulation PER-7/PJ/2025 — explicitly allow companies to register for VAT (PKP) using a virtual office, provided certain conditions are met.

So the question is no longer: “Is a virtual office legal?”

The real question for investors entering Bali’s hospitality and residential tourism market is: “Will a virtual office structure support my business once it becomes operational?”

Incorporation vs Operation: Where Investors Get Caught

A virtual office will typically allow a company to pass:

✔️ AHU Registration

✔️ Deed of Establishment

✔️ NIB issuance through OSS

This gives investors a sense of regulatory comfort early in the process. However, Bali’s regulatory system does not assess risk at incorporation. It assesses risk at the point of:

▪ VAT registration (PKP)

▪ Tourism licensing (TDUP)

▪ Building Function Certification (SLF)

▪ Environmental approvals

▪ Local operational enforcement

This is where many virtual-office-based structures begin to encounter friction.

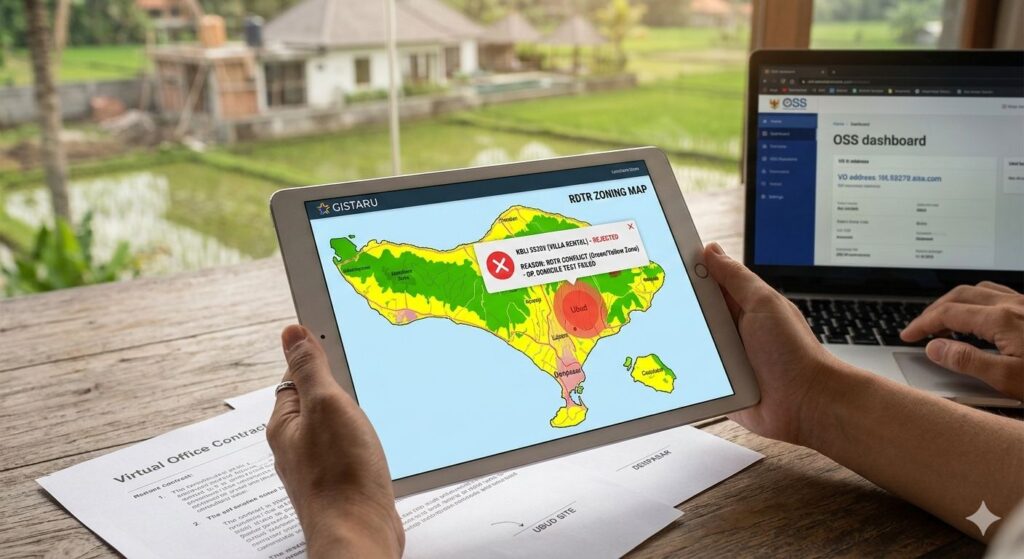

RDTR Zoning and the “Place of Activity” Test

Indonesia’s spatial planning framework requires business activity to align with regional zoning (RDTR), which is now integrated into OSS licensing under the risk-based licensing regime introduced by PP 28/2025.

In practice, this means:

A consultancy PMA operating from a VO in Denpasar may be acceptable. But a PT PMA with:

▪ KBLI 55203 (Villa Rental)

▪ KBLI 55106 (Non-Star Hotel)

▪ KBLI 55204 (Serviced Apartment)

… domiciled in a virtual office, while operating villas in Ubud, Tabanan or Uluwatu, may face rejection at the PKP or tourism licensing stage. Why?

Because under Indonesian tax law, corporate domicile is not determined solely by formal address — but by the actual place where business activity occurs. If the declared address does not reasonably reflect operational reality, licensing and tax registration may be denied or delayed.

PER-7/PJ/2025: Virtual Offices and PKP

Recent updates now allow virtual offices to be used as PKP registration locations — but only if:

▪ The VO provider is itself PKP-registered

▪ A physical working space is provided

▪ A minimum one-year lease agreement is in place

▪ The company’s KBLI logically supports office-based activity

▪ The company conducts real activity at the VO

▪ The company has only one place of business activity

This becomes critical for hospitality-linked investments.

If your company’s real economic activity occurs at a villa, resort, or accommodation unit, the tax authority may require PKP registration at that operational location — not the VO.

Short-Term Rental Licensing: A Structural Limitation

In Bali’s current enforcement environment, most short-term rental operations require licensing tied to:

▪ The physical property

▪ Its zoning classification

▪ Its environmental approval

▪ Its building function certification

Foreign-owned PT PMAs frequently cannot obtain these licenses directly for short-term accommodation activities. As a result, many STR-based investment models now rely on:

A locally owned PT PMDN operator working alongside the investment-holding PMA structure. Each structure must be assessed individually to ensure compliance across tax, zoning, and licensing frameworks.

The Formalising Market Ahead

For years, Bali’s property market allowed incorporation-stage compliance to stand in for operational legality.

That distinction is narrowing.

With OSS increasingly integrated with spatial planning data and local enforcement now focused on misuse of residential zones for tourism activity, the difference between:

▪ Administrative domicile

▪ Operational business location

is becoming legally significant. A virtual office may still be a valid entry point. But it is no longer a guarantee of downstream licensing readiness.

How Seven Stones Can Help

At Seven Stones, we assist investors in structuring their Indonesian entry based not only on incorporation requirements — but on long-term operational viability. This includes:

▪ PMA and PMDN structuring

▪ Zoning and KKPR due diligence

▪ PKP readiness

▪ Tourism licensing pathways

▪ Management company integration

Each investment model requires a tailored approach, particularly where residential tourism or short-term rental activity is involved.

In today’s Bali market, legality begins at incorporation — but compliance is tested at operation.